Business fund raising is the process by which entrepreneurs secure capital from diverse sources to finance growth, hire talent, and reach the milestones that make a business worth backing. The industry term is “capital raising,” and both phrases describe the same discipline. Getting it right requires more than a polished pitch deck. VC fundraising typically takes 3–6 months to close, while traditional bank loans run 60–90 days and alternative lenders can move in 24–72 hours. Knowing which route fits your stage, and preparing accordingly, is what separates founders who close rounds from those who run out of runway.

What financial planning do you need before business fund raising?

Preparation is not optional. Investors reject founders who cannot explain their burn rate, runway, or the precise milestone their raise will fund. Get these numbers right before you speak to a single investor.

Burn rate and runway

Your monthly burn rate is total cash out minus total cash in. Divide your current cash balance by that figure and you get your runway in months. Founders should target 18–24 months of runway, plus a 20% buffer for safety. That buffer matters because fundraising always takes longer than expected, and running a process on four months of cash is a negotiating disaster.

| Metric | Formula | Target |

|---|---|---|

| Monthly burn rate | Total monthly outgoings minus monthly revenue | Know this to the pound |

| Runway (months) | Cash balance divided by monthly burn | 18–24 months |

| Safety buffer | Runway multiplied by 1.2 | Built into your raise amount |

| Fundraising start trigger | When runway hits 9–12 months | Begin process immediately |

Valuation benchmarks

Valuation is not a number you invent. Pre-seed and angel rounds carry standard post-money valuation caps of £5M–£10M (broadly equivalent to the $6M–$12M benchmark). Series A rounds typically raise £6M–£12M, anchored to annual recurring revenue of £800K–£2.5M. Knowing these benchmarks stops you from pricing yourself out of the market or giving away too much equity too early.

Pro Tip: Build your financial model before you set your valuation. The model reveals what you actually need to raise, which then informs the valuation conversation, not the other way around.

Solid financial forecasting also signals credibility. Investors want to see a 36-month model with clear assumptions, not a spreadsheet built the night before the pitch. A documented financing strategy aligned to 3–10 year milestones consistently reduces your cost of capital over time. That is the standard serious founders hold themselves to.

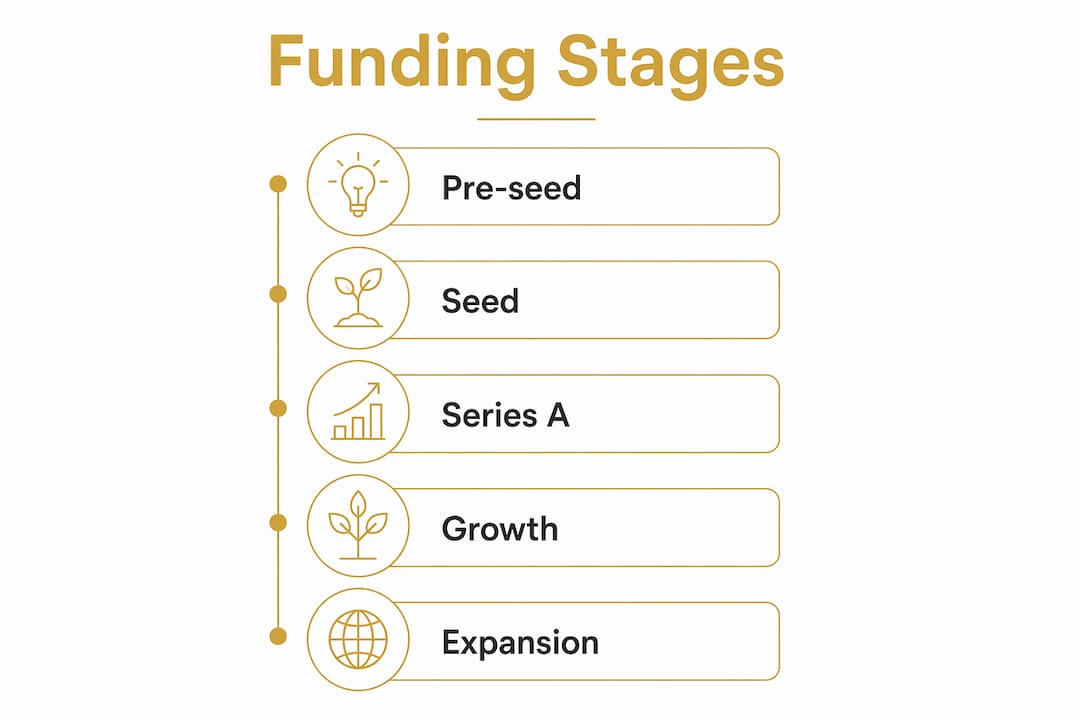

Which funding sources work best at each business stage?

The right funding source depends on your stage, your revenue, and how much equity you can afford to give away. Capital raising is not a single decision. It is a sequence.

Non-dilutive options first

Non-dilutive funding preserves your ownership and should always be your first port of call. Options include:

- Grants: Innovate UK, the British Business Bank, and sector-specific grant programmes offer non-repayable capital. Competition is high, but the cost is zero equity.

- Crowdfunding: Platforms like Seedrs and Crowdcube let you raise from a crowd of smaller investors. This also builds a community of advocates for your product.

- Revenue-based financing (RBF): You repay a fixed percentage of monthly revenue until a cap is reached. The RBF market has grown to $5.8 billion globally and is expanding at nearly 70% annually. That growth reflects how many founders now prefer it over dilutive equity at early stages.

Non-dilutive funding options like grants, pre-sales, and RBF serve as deliberate stepping stones before equity funding. Use them to reach a milestone that makes your equity worth more.

Equity funding: angels and venture capital

Angel investors typically write cheques of £25K–£250K and are most active at pre-seed. Venture capital firms enter at seed or Series A, expecting traction, a repeatable sales motion, and a credible founding team. Understanding valuation caps and deal sizes at each stage prevents costly mistakes in term sheet negotiations.

Capital stacking for small businesses

Capital stacking is the deliberate layering of complementary financing products to maximise available capital at the lowest blended cost. The four-layer structure runs as follows: a bankability foundation (your credit profile and trading history), working capital revolvers (invoice finance or overdraft facilities), term debt (bank loans or government-backed schemes), and specialty financing (grants, RBF, or equity). Building cheapest capital first preserves your creditworthiness for future rounds.

| Funding type | Stage | Dilutive? | Speed | Best for |

|---|---|---|---|---|

| Grants | Pre-seed to growth | No | Slow (months) | R&D, innovation projects |

| Revenue-based financing | Revenue-generating | No | Fast (days) | Working capital, marketing |

| Angel investment | Pre-seed to seed | Yes | Medium (weeks) | Early traction, networks |

| Venture capital | Seed to Series A+ | Yes | Slow (3–6 months) | High-growth, scalable models |

| Bank loans | Established businesses | No | Medium (60–90 days) | Asset purchase, expansion |

How do you build an effective fundraising process?

A fundraising process is a sales process. Treat it with the same discipline you apply to your pipeline.

Choosing the right instrument: SAFEs vs priced rounds

At pre-seed and seed, use a Simple Agreement for Future Equity (SAFE). Legal costs for priced rounds run £12K–£20K; SAFEs cost £1.5K–£4K. That difference is real money for an early-stage company. SAFEs also close faster, which matters when investor sentiment can shift in weeks.

The fundraising process step by step

- Decide to raise. Define the milestone your capital will fund. Raising without a clear milestone destroys credibility.

- Build your materials. Prepare a pitch deck, a financial model, and a data room. Your investor-ready metrics must be current and defensible.

- Research investors. Build a tiered list. Tier A is your dream investors. Tier B is strong but not your first choice.

- Get warm introductions. Warm introductions convert investors 10 times better than cold outreach. That figure alone should reshape how you spend your networking time.

- Run meetings in batches. Schedule 8–10 investor meetings per week, starting with Tier B investors. Refine your pitch on Tier B before you sit down with Tier A.

- Create urgency. Once you have a term sheet or strong verbal commitment, communicate it. Investors move faster when they believe others are moving too.

- Close and complete diligence. Share information in a controlled sequence. Do not hand over your full data room before a term sheet is signed.

Pro Tip: Start your fundraise with Tier B investors deliberately. The feedback sharpens your pitch, and the momentum signals to Tier A that the round is moving. This is not dishonest. It is process management.

Raising capital aligned to milestones rather than as an end in itself keeps your focus on execution. The raise is a means to reach the next stage, not the achievement itself.

What are the most common fundraising mistakes to avoid?

Most fundraising failures are predictable. The errors repeat across founders and stages.

- Raising too early. Without product-market fit or meaningful traction, you will either fail to close or accept punishing terms. Investors price uncertainty into your valuation.

- Raising too much at too high a valuation. A bloated valuation creates a down-round risk at your next raise. Down rounds destroy morale and signal distress to the market.

- Pitching without batching. Serial pitching without batch scheduling kills momentum. If you drip meetings out over three months, you never build the competitive pressure that closes deals.

- Ignoring non-dilutive options. Founders who go straight to equity give away ownership they could have preserved with a grant or RBF facility.

- Entering diligence unprepared. Investors who find inconsistencies in your data room walk away. Prepare your financials, cap table, and legal documents before the first meeting.

Pro Tip: Track every investor conversation in a CRM, even a simple spreadsheet. Knowing who said what, and when, stops you from sending the same update twice or missing a follow-up that could have closed the round.

“The founders who close rounds fastest are not the ones with the best ideas. They are the ones who run the tightest process, know their numbers cold, and treat investor relations like a professional sales function.”

Aligning your raise with realistic milestones also protects you from the trap of raising capital you cannot deploy productively. Capital without a plan is expensive noise.

Key takeaways

Business fund raising succeeds when founders combine rigorous financial preparation, a sequenced funding strategy, and a disciplined investor process built around warm introductions and batched meetings.

| Point | Details |

|---|---|

| Plan runway before you raise | Target 18–24 months of runway plus a 20% buffer before approaching investors. |

| Use non-dilutive funding first | Grants, crowdfunding, and revenue-based financing preserve equity for later, higher-value rounds. |

| SAFEs save money at early stages | SAFE agreements cost a fraction of priced rounds and close faster for pre-seed and seed raises. |

| Warm introductions outperform cold outreach | Investor introductions through trusted connections convert 10 times better than unsolicited approaches. |

| Batch your investor meetings | Running 8–10 meetings per week creates urgency and sharpens your pitch before Tier A conversations. |

Why fundraising is a tool, not a trophy

I have worked with founders at every stage, from pre-revenue startups to SaaS businesses approaching Series A, and the pattern is consistent. The ones who struggle treat the raise as the goal. The ones who succeed treat it as a mechanism to reach a specific milestone, whether that is £1M ARR, a product launch, or a new market entry.

The sequencing of capital sources matters more than most founders realise. Cheap capital first, equity last. A business that has used grants, RBF, and invoice finance before approaching a VC arrives with a lower cost of capital, a cleaner cap table, and a stronger negotiating position. That is not theory. That is what I see in practice.

In 2026, investor expectations have tightened. Metrics need to be current, defensible, and presented in a format investors recognise. A fractional CFO onboarding roadmap can close the gap between where your financials are and where they need to be before you enter a process. The founders who invest in that preparation close rounds. The ones who skip it spend six months in diligence hell.

My honest advice: do not start a fundraising process until you can answer three questions without hesitation. What is your monthly burn? What milestone does this raise fund? What does your business look like at the end of that runway? If any of those answers are vague, fix the model before you book the first meeting.

— Kishen Patel

How Consult EFC supports your capital raising process

Raising capital is a financial discipline, not just a sales exercise. Consult EFC works with UK startups and scaleups to build the financial models, investor-ready metrics, and funding strategies that give founders a real advantage in a competitive market.

Kishen Patel and the Consult EFC team bring ICAEW-level rigour to every engagement, from fractional CFO services for startups preparing for their first institutional round to SaaS businesses targeting Series A. Whether you need a financial model built from scratch, a cap table reviewed, or a funding strategy aligned to your 24-month plan, Consult EFC delivers the depth of a Big Four firm without the full-time cost. Contact Consult EFC to prepare your raise properly before the first investor meeting.

FAQ

What is business fund raising?

Business fund raising, or capital raising, is the process of securing external finance from investors, lenders, or grant bodies to fund business growth. It includes equity investment, debt, grants, and non-dilutive instruments like revenue-based financing.

How long does fundraising typically take?

VC fundraising takes 3–6 months on average, bank loans require 60–90 days, and alternative lenders can fund in 24–72 hours. Timeline depends on your stage, preparation, and the instrument you are using.

What is the difference between a SAFE and a priced round?

A SAFE is a simple agreement that converts to equity at a future round, costing £1.5K–£4K in legal fees. A priced round sets a fixed valuation immediately and costs £12K–£20K in legal fees, making SAFEs the preferred choice for early-stage raises.

How much runway should I have before raising?

Founders should target 18–24 months of runway, plus a 20% buffer. Starting your fundraising process when you have 9–12 months of cash remaining gives you enough time to run a proper process without negotiating from a position of desperation.

What is capital stacking?

Capital stacking is the practice of layering multiple financing products, from bank facilities to grants to equity, to maximise available capital at the lowest blended cost. The four-layer model prioritises the cheapest sources first, preserving equity for when it delivers the highest return.

Recommended

Not sure where your business stands right now?

Book a free 30-minute call with Kish. Bring your numbers, your questions, or just your situation. You will leave with a clearer picture than you arrived with.

Book a Free Strategy Call

Over 12 years across Big Four audit, Investment Banking, and corporate advisory. Kish works with SaaS founders, tech companies, and ambitious UK SMEs from £1M to £50M in revenue on fundraising, valuations, exit planning, and financial strategy. ICAEW regulated. Big Four trained. Based in London.