An investor due diligence financial model is a structured, scenario-driven analytical tool used to verify a business’s financial health, validate assumptions, and assess investment risk before capital is committed. It is the primary instrument through which investors and financial analysts interrogate projections, stress test unit economics, and confirm that management’s narrative is grounded in operational reality. Financial model gaps and unit economics issues account for more than 50% of deal complications during Series A and B fundraising, outpacing legal and HR challenges combined. That single statistic explains why building a model that withstands rigorous scrutiny is not optional. It is the foundation of any credible investment evaluation process.

What components make a robust investor due diligence financial model?

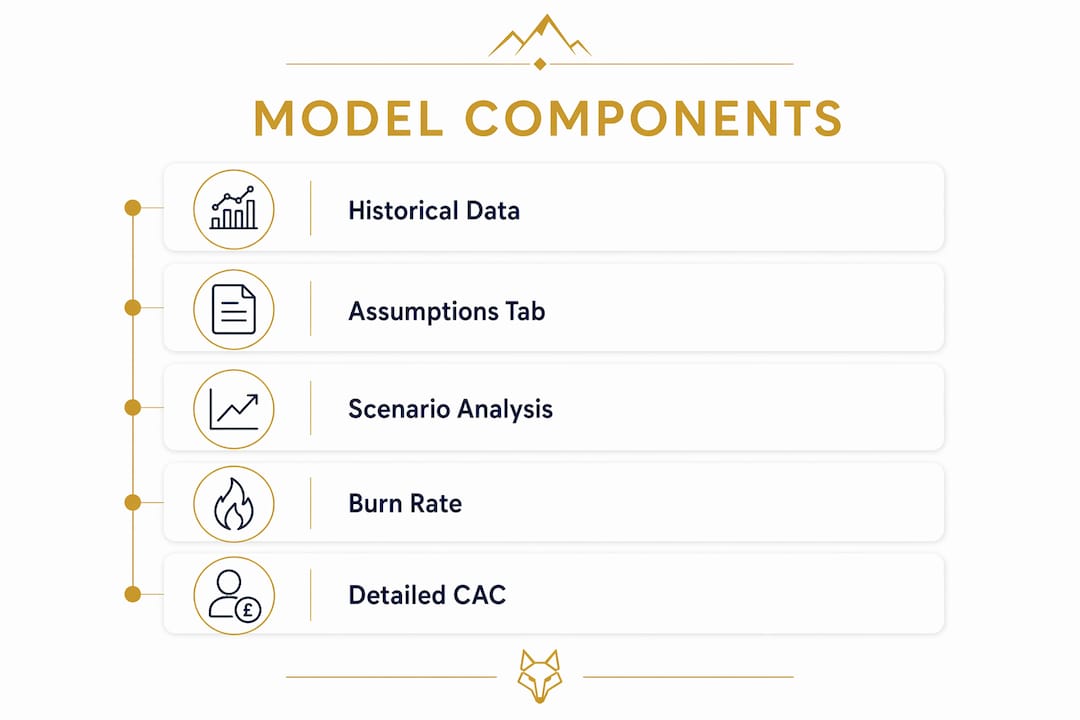

A model that survives investor scrutiny is built on five non-negotiable components. Each one serves a distinct purpose in the financial model analysis process, and missing any one of them signals to investors that management lacks financial discipline.

Historical financial data forms the baseline. Investors expect at minimum 24 months of profit and loss, balance sheet, and cash flow statements presented in a clean, consistent format. This historical record allows analysts to identify trends, seasonality, and anomalies before they ever look at a forward projection.

An explicit assumptions tab is where credibility is won or lost. Every input driving the model must be listed with its source, the date it was last reviewed, and the confidence level assigned to it. Investors prioritise the assumption log rather than final output numbers, because assumptions reveal whether management truly understands its own business. An assumption without an owner is a liability in a due diligence meeting.

Three scenarios with granular timeframes are now a baseline expectation, not a differentiator. Investor-ready models for Series A and B must include base, upside, and downside cases with monthly granularity for year one and quarterly for years two and three. A model presenting only a single optimistic case reads as a marketing document, not a decision-making tool.

An integrated three-statement model connects the income statement, cash flow statement, and balance sheet so that every operational change flows through to its financial consequence. Cash flow reconciliation and integrated three-statement models demonstrate management’s grasp of financial interdependencies. Without this integration, a model cannot be trusted to reflect reality.

Key performance indicators relevant to the business model must be embedded and reconciled to the financials. For SaaS businesses, that means customer acquisition cost (CAC), lifetime value (LTV), net revenue retention (NRR), burn rate, and runway. For product businesses, gross margin by SKU and inventory turns matter. The KPIs must not float independently; they must tie directly to the revenue and cost drivers in the model.

- Historical P&L, balance sheet, and cash flows covering at least 24 months

- Dedicated assumptions tab with source, date, and confidence level for every input

- Base, upside, and downside scenarios with monthly and quarterly granularity

- Fully integrated income statement, cash flow, and balance sheet

- SaaS or sector-specific KPIs reconciled to model outputs

- Headcount schedule driving salary costs and linked to hiring plan

- CAC broken down by acquisition channel, not blended across all sources

Pro Tip: Build your burn rate from a headcount schedule rather than a single cost line. Break CAC by channel so investors can see which growth levers are efficient and which are subsidised. These two changes alone transform a model from a summary into a credible operational plan.

How do investors scrutinise financial models during due diligence?

Investor scrutiny during due diligence follows a predictable sequence. Understanding that sequence allows you to pre-empt the most common objections before they arise in a live meeting.

- Structure audit. The first thing an experienced analyst checks is whether the model separates inputs, calculations, and outputs. The D-I-O framework (Data, Inputs, Outputs) is the standard reference point. The fastest audits start with structure and clear separation of assumptions, formulas, and outcomes. A model where assumptions are scattered across formula cells signals that the builder does not understand modelling hygiene.

- Formula integrity check. Analysts scan for hardcoded values embedded in formula cells, broken links, and circular references. Circular references in debt interest modelling undermine model stability and erode investor confidence immediately. A single circular reference in a debt schedule can cause the entire model to return incorrect outputs under scenario changes.

- Assumption traceability. Every material input is traced back to its source. Investors ask: where did this growth rate come from? What is the basis for this churn assumption? If the answer is not documented in the model, the founder must answer verbally, which introduces inconsistency and doubt.

- Scenario stress testing. Investors test models by tweaking key assumptions; models not built with scenario infrastructure fail quickly under this pressure. A model that requires manual changes to 40 cells to run a downside case is not a scenario model. It is a single-case model with extra steps.

- Independent rebuild. Sophisticated investors or their advisers will rebuild portions of the model independently using the same inputs. If their outputs differ from yours, the model has errors. This is not a theoretical risk. It happens regularly in Series A and B processes.

Common pitfalls that cause models to fail investor scrutiny include flat burn assumptions that ignore hiring plans, inconsistent unit economics across cohorts, and runway calculations that do not reconcile to the cash flow statement. Each of these signals that the model was built to tell a story rather than to reflect operational reality.

Pro Tip: Run a 30-minute final audit before sharing any model with an investor. Check tab order, confirm all headers are present, remove every hardcoded value from formula cells, and verify that your three scenarios produce materially different outputs. A structured final audit directly improves investor confidence and reduces delays in the diligence process.

Top-down vs driver-based: which modelling approach wins?

The choice of modelling methodology is not a technical preference. It is a credibility signal. Investors read the approach as evidence of how well management understands its own growth engine.

| Approach | Key feature | Benefit | Pitfall |

|---|---|---|---|

| Top-down forecasting | Market size percentage capture | Simple to communicate | Disconnected from operational reality |

| Driver-based revenue build | Inputs tied to sales capacity, conversion rates, pricing | Traceable and defensible | Requires detailed operational data |

| Single-case model | One set of assumptions | Fast to build | Reads as optimistic marketing |

| Multi-scenario model | Base, upside, downside toggles | Demonstrates risk awareness | Requires scenario infrastructure |

| Manual assumption changes | Direct cell edits per scenario | Flexible | Error-prone and inconsistent |

| Dynamic scenario toggles | Dropdown or switch-driven | Audit-friendly and repeatable | Requires upfront build investment |

Top-down forecasting, where revenue is derived from capturing a percentage of a total addressable market, is the weakest approach in a due diligence context. It is not traceable to any operational metric and cannot be stress tested meaningfully. An investor who asks “how does your sales headcount support this revenue number?” will find no answer in a top-down model.

Driver-based revenue modelling links projections directly to operational inputs: number of sales representatives, average deal size, sales cycle length, conversion rates by stage, and pricing tier mix. This approach allows investors to interrogate each assumption independently and understand which variables carry the most risk. For SaaS businesses, the financial modelling and forecasting process should connect monthly recurring revenue growth directly to new logo acquisition, expansion revenue, and churn by cohort.

Investor diligence increasingly demands scenario robustness and transparent, defensible assumptions rather than optimistic single-case forecasts. A dynamic scenario toggle, built as a dropdown cell that switches all assumptions simultaneously, is far superior to a model where scenarios require manual edits. The toggle approach is auditable, repeatable, and demonstrates that the builder anticipated investor behaviour.

Best practices for building investor-ready models in 2026

The difference between a model that accelerates due diligence and one that stalls it often comes down to presentation and documentation discipline, not the sophistication of the underlying maths.

Strong financial models accelerate diligence by reducing the time investors spend verifying numbers and increasing the proportion of meetings spent on strategic discussion. The practical implication is that every hour invested in model hygiene before a process begins saves multiple hours of back-and-forth during it.

- Organise model tabs in logical order: cover sheet, assumptions, revenue build, cost build, headcount, three statements, KPI dashboard, scenarios

- Use blue font for all input cells and black font for all formula cells. Colour coding inputs versus formulas reduces errors and makes the model immediately legible to any analyst

- Maintain an assumption log as a dedicated tab, updated with source, date, and confidence level every time an assumption changes

- Reconcile runway explicitly to the cash flow statement so that the headline number is not floating independently of the model

- Stress test at least three key variables in isolation: growth rate, gross margin, and churn. Understand the output range before an investor asks

- Align financial KPIs to operational metrics so that a change in sales headcount flows through to pipeline, revenue, and cash within the same model

Tools matter here. Excel remains the standard for institutional-grade modelling, with Google Sheets used for collaborative early-stage work. For SaaS businesses, templates built around cohort analysis and monthly recurring revenue waterfalls save significant build time and reduce structural errors. The SaaS financial transformation roadmap at Consult EFC provides a structured approach to building these models from the ground up.

Pro Tip: Assign a named owner to every material assumption in your log. When an investor asks why your churn rate is 2% rather than 5%, the person who owns that assumption should be able to defend it with data. Assumption ownership converts a spreadsheet into an accountable management tool.

Key takeaways

A credible investor due diligence financial model requires integrated three-statement architecture, documented assumption ownership, and dynamic scenario infrastructure to withstand rigorous 2026 fundraising scrutiny.

| Point | Details |

|---|---|

| Assumption ownership is critical | Every material input must have a named owner, source, and confidence level documented in a dedicated log. |

| Three scenarios are the minimum | Base, upside, and downside cases with monthly granularity for year one are now a baseline investor expectation. |

| Structure signals credibility | Separating inputs, calculations, and outputs using the D-I-O framework accelerates audit and builds trust. |

| Driver-based models outperform top-down | Linking revenue to operational metrics makes projections traceable and defensible under investor questioning. |

| Pre-sharing audit prevents delays | A 30-minute structural check before submission removes the most common errors that stall due diligence. |

Why most financial models fail the moment scrutiny begins

After working with founders and analysts across dozens of fundraising and acquisition processes, the pattern is consistent. The models that fail do not fail because the numbers are wrong. They fail because the structure does not support interrogation.

A founder who has built a model to tell a story will find that story unravels the moment an investor changes a single assumption. The revenue line does not move. The burn stays flat. The runway does not reconcile. These are not modelling errors in the narrow technical sense. They are symptoms of a model that was never designed to be a decision-making tool.

The misconception I encounter most often is that a financial model is a fundraising document. It is not. It is a management instrument that happens to be shared with investors. The distinction matters because it changes how you build it. A fundraising document is polished and static. A management instrument is transparent, dynamic, and built to absorb challenge.

The future of financial modelling in due diligence is moving towards greater automation and AI-assisted data population, with tools beginning to pull actuals directly from accounting systems into model structures. But the underlying discipline remains unchanged. Investors want to see that management understands the operational drivers of its own business. No amount of automation substitutes for that understanding.

The founders and finance teams who invest in model quality before a process begins consistently close faster and on better terms. That is not a coincidence. It reflects the fact that models acting as decision-making systems reduce the information asymmetry that makes investors cautious. Reduce that asymmetry, and you change the negotiating dynamic entirely.

— Kish Patel

How Consult EFC prepares your model for investor scrutiny

Building a model that passes rigorous investor scrutiny requires more than a good spreadsheet. It requires the kind of financial leadership that most scaling businesses do not have in-house at the point they need it most.

Consult EFC provides fractional CFO services specifically designed for high-growth SaaS companies and ambitious UK SMEs preparing for fundraising or sale. The team brings ICAEW-credentialled expertise to financial model construction, scenario architecture, and assumption documentation, at a fraction of the cost of a full-time CFO hire. For businesses that need their cash flow projections to hold up under investor questioning, Consult EFC’s cash flow forecasting service builds the granular, defensible outputs that accelerate due diligence and support stronger valuations. If your next fundraising round or exit is on the horizon, the time to build the model is now.

FAQ

What is an investor due diligence financial model?

An investor due diligence financial model is a structured analytical tool used to verify a business’s financial health, validate assumptions, and assess investment risk before capital is committed. It typically includes integrated three-statement financials, scenario analysis, and a documented assumption log.

What scenarios should a due diligence financial model include?

A model prepared for Series A or B due diligence must include base, upside, and downside scenarios with monthly granularity for year one and quarterly granularity for years two and three. Single-case models are treated as marketing documents rather than credible investment tools.

Why do investors focus on assumptions rather than output numbers?

Investors interrogate assumptions because outputs are only as reliable as the inputs driving them. Mapping every assumption to its source and confidence level speeds the due diligence process and demonstrates that management understands its own operational drivers.

What are the most common financial model errors during due diligence?

The most frequent errors include circular references in debt schedules, hardcoded values embedded in formula cells, flat burn assumptions that ignore hiring plans, and runway figures that do not reconcile to the cash flow statement.

How does a driver-based model differ from a top-down forecast?

A driver-based model links revenue projections directly to operational metrics such as sales headcount, conversion rates, and pricing, making each assumption traceable and defensible. A top-down forecast derives revenue from market share capture and cannot be stress tested against operational constraints.

Recommended

Not sure where your business stands right now?

Book a free 30-minute call with Kish. Bring your numbers, your questions, or just your situation. You will leave with a clearer picture than you arrived with.

Book a Free Strategy Call

Over 12 years across Big Four audit, Investment Banking, and corporate advisory. Kish works with SaaS founders, tech companies, and ambitious UK SMEs from £1M to £50M in revenue on fundraising, valuations, exit planning, and financial strategy. ICAEW regulated. Big Four trained. Based in London.