A business sale can stall when the buyer sees risk and the seller sees upside. The founder points to a booming pipeline; the buyer worries the forecasts are too optimistic. That is where an earn-out comes in.

In simple terms, part of the purchase price is paid on completion, and part is paid later – only if the business hits agreed targets. In UK private company sales, this structure bridges valuation gaps, reduces upfront risk for the buyer, and keeps both sides at the table.

Done well, an earn-out makes a deal happen. Done badly, it stores up bitter arguments for later. The detail in the legal wording, the financial metrics, and the tax treatment matters far more than the headline price.

Selling your business? Don’t let an earn-out trap your exit value. Book a free Strategy Call with Consult EFC to ensure your deal structure is safe, clear, and achievable.

What an earn-out actually is and when it is used

An earn-out is deferred consideration linked to future performance. The buyer pays a fixed sum on day one, then pays more if the business meets agreed results after completion.

That structure is common in private M&A because the future is often the hardest part to price. A founder may point to a strong pipeline, high retention, or a product about to scale. The buyer may accept the potential, but still worry that forecasts are too optimistic. An earn-out lets both sides move forward without settling every argument up front.

In the UK, this is often seen in founder-led businesses, service firms, and growth companies where value depends on momentum after the deal closes. It can also help where bank funding is tight, because the buyer spreads part of the price over time.

Recent market conditions have made this even more relevant. As M&A buyers have become more cautious and selective, more deals are being pushed toward deferred pricing structures.

How the payment structure usually works

Most earn-outs run for one to three years. During that period, the business is measured against agreed targets. If it hits them, the seller receives extra consideration.

The trigger can be based on revenue, EBITDA, profit, customer retention, contract wins, or other milestones. Some deals pay the full earn-out only if a threshold is met. Others use a formula, so higher performance increases the payout.

The detail matters. A seller needs to know what counts as revenue, when income is recognised, which costs can be charged, and how the accounts will be prepared. Without that, the formula can look clear but still produce disputes.

Which UK deals tend to use earn-outs

Earn-outs are most common where value is hard to pin down at completion. That includes high-growth SaaS businesses, agencies, healthcare providers, specialist professional services firms, and companies where a few key customers drive results.

They also appear when the seller is expected to stay on. If the founder will lead the business for another 12 to 24 months, the buyer often wants part of the price tied to what happens in that period.

Where the business is stable, asset-heavy, and easy to forecast, earn-outs are less common. By contrast, where performance depends on key people, product launches, or fast sales growth, they are much more likely.

The most common earn-out structures in UK M&A

There is no single model. Earn-outs are flexible, and the structure should fit the business rather than copy the last deal someone saw.

At a high level, most arrangements fall into three groups: financial targets, payment curves, and milestone-based events. Each shifts risk in a different way.

Targets based on revenue, profit, or EBITDA

Revenue is often the easiest measure to understand. It is top-line, visible, and harder to alter through accounting judgement. That makes it attractive where the parties want simplicity.

Profit and EBITDA can track value more closely, but they create more room for argument. Costs can move between periods. Central charges may be added. Integration decisions can affect margins. One party may see those changes as normal management, while the other sees them as value leakage.

This quick comparison shows the trade-off:

| Measure | Main benefit | Main risk |

|---|---|---|

| Revenue | Simple and easy to track | Can reward low-margin sales |

| Profit | Closer to cash outcome | Sensitive to cost allocation |

| EBITDA | Common in deal pricing | Open to adjustments and policy choices |

In practice, the cleaner the metric, the easier the earn-out is to live with.

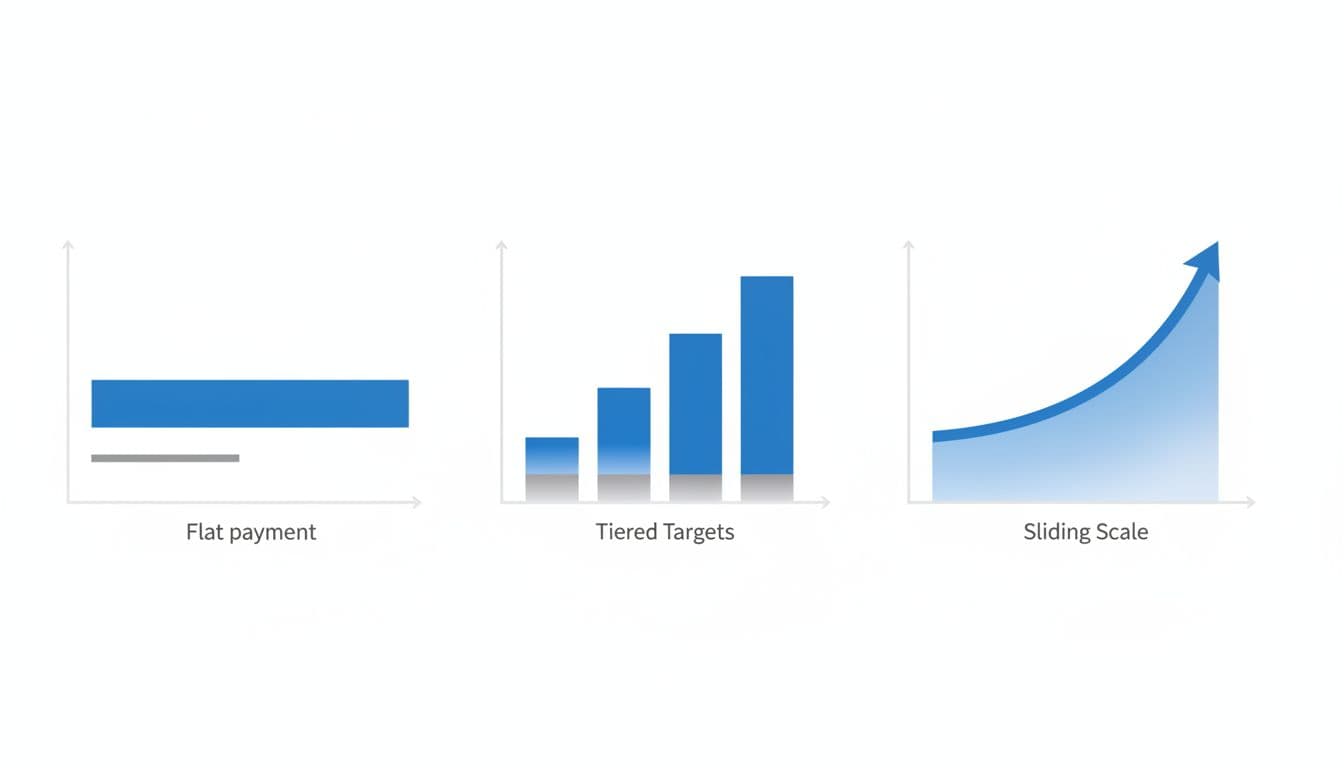

Fixed payments, tiered payments, and sliding scales

A fixed earn-out is the bluntest tool. Hit the target and the seller gets the payment. Miss it and the seller gets nothing. That is simple, but it can feel harsh if performance falls just short.

Tiered payments soften that edge. For example, 80 per cent of target might unlock part of the earn-out, while 100 per cent unlocks the full amount. That reduces cliff-edge risk.

Sliding scales go further. The payment rises with performance under a formula. These can be fairer, because they reflect actual results more closely. However, they also need tighter drafting and better reporting.

Milestone-based earn-outs for special situations

Some businesses do not fit neat financial targets. A biotech company may depend on regulatory approval. A SaaS company may be valued on landing a major enterprise contract. A manufacturing business may hinge on a product launch or framework renewal.

In those cases, milestone-based earn-outs can work better than pure financial tests. The event must still be defined with care. If the target is “sign a major customer”, the SPA should say what counts as major, when the contract counts, and whether later termination changes the outcome.

Why buyers and sellers agree to earn-outs, and where the risk sits

Earn-outs survive because they can solve a real commercial problem. The buyer wants protection against overpaying. The seller wants credit for future upside. Both points can be valid at the same time.

How earn-outs can help buyers

For buyers, the first benefit is price protection. If future growth does not arrive, they do not pay for it.

They also help with funding. Paying part of the consideration later can reduce the cash needed on completion. That matters in lower mid-market deals, where funding conditions can tighten quickly.

There is also a behavioural benefit. If the founder stays on, the earn-out can keep attention on growth, customer retention, and execution after closing.

How earn-outs can help sellers

For sellers, an earn-out can preserve value when the buyer will not meet the headline price on day one. Instead of cutting the valuation now, the seller keeps the chance to receive more later.

This can be useful where the business is growing fast, but the buyer wants proof. It can also unlock a deal that would otherwise fail because both sides are too far apart on price.

If the targets are fair and the seller still influences performance, the total proceeds can exceed an all-cash offer made on a more cautious valuation.

The main downsides to watch

The risk starts the moment control changes hands. After completion, the buyer usually runs the business. Yet the seller’s deferred price may still depend on what happens next.

That can create tension over spending, hiring, pricing, integration, and strategy. A buyer may make sensible long-term decisions that reduce short-term earn-out performance. A seller may feel punished for choices they no longer control.

Most earn-out disputes are not about bad faith. They start because the document left too much open to interpretation.

There is also a wider commercial risk. If targets are badly designed, management may chase short-term numbers and ignore the health of the business.

The clauses that need the most attention in the SPA

In UK deals, the share purchase agreement is where an earn-out succeeds or fails. The commercial idea may be sound, but unclear drafting can undo it.

How performance should be measured

The first job is to define the metric properly. If the earn-out is based on revenue, the SPA should say how revenue is recognised, which contracts count, whether intercompany sales are excluded, and what happens to refunds or credits.

If the measure is EBITDA or profit, the drafting needs even more care. Which accounting policies apply? Can the buyer change them? Are exceptional costs added back? Can head office charges be allocated to the target business?

Those points sound technical, but they decide whether the seller gets paid.

What the buyer can and cannot do after completion

This is often the hardest negotiation. Sellers want protection against changes that reduce the earn-out unfairly. Buyers want freedom to run the business.

The answer is usually a middle ground. The SPA might restrict major restructurings, unusual cost allocations, asset transfers, or business changes that target the earn-out period. It may also require the buyer to operate in good faith or in the ordinary course, although those words still need careful drafting.

A seller may also ask for board access, monthly reporting, and rights to review working papers. Those are not minor points. They are how the seller checks whether the numbers reflect the deal.

Related Resource: Don’t let accounting tricks derail your deal. Read our guide on the Quality of Earnings Preparation.

How disputes are handled if the numbers do not agree

Even strong drafting cannot remove every disagreement. The SPA should set out a fast route to resolution.

Often that means expert determination by an independent accountant. The process should state what can be referred, the timetable, who pays, and whether the expert decides only accounting points or wider legal issues as well.

Without that mechanism, a dispute can drift into a long and expensive fight. That helps nobody.

Tax and accounting points UK sellers should not ignore

The legal price and the after-tax outcome are not the same. Sellers sometimes focus so hard on the headline number that they overlook the structure.

Capital gains tax and Business Asset Disposal Relief

Earn-out proceeds are often taxed as capital rather than income, but the treatment depends on the facts and the way the consideration is structured. That distinction matters because capital treatment may be more favourable than income tax.

Business Asset Disposal Relief may also be available in some cases, subject to the conditions in force at the time and the seller’s own position. Sellers should not assume relief applies. They need advice early, before terms harden.

Why timing and structure can affect the final outcome

Tax can bite before cash is received. In some cases, the seller may need to value the earn-out right at completion for tax purposes, even though the actual payment will only be known later.

That can create a cash flow problem. It can also change the economics of the deal if the earn-out proves hard to collect or pays later than expected.

Accounting treatment matters too. Clear forecasts, supportable assumptions, and a sensible valuation of deferred consideration can help avoid surprises with investors, auditors, or HMRC.

How to negotiate a fair earn-out without killing the deal

A good earn-out is commercial first and legal second. If the structure does not fit how the business works, better drafting will not save it.

Choose targets that are clear and hard to manipulate

Simple targets are usually better. If both sides can measure them easily, they are more likely to trust the result.

That does not mean the metric must be crude. It means it should be observable, defined, and tied to value. In many SME and SaaS deals, that points towards revenue quality, recurring income, customer retention, or a tightly drafted EBITDA measure.

Match the earn-out period to the business cycle

The time frame should reflect how the business proves value. A 12-month period may work for a stable services business with recurring revenue. It may be too short for enterprise software with long sales cycles, or for a company where contract renewals fall in uneven waves.

If the period is too short, the seller carries timing risk. If it is too long, both sides stay tied together longer than they want.

Build in seller protections where they are needed

Seller protections are not about mistrust. They are about keeping the pricing mechanism fair after control passes.

Useful protections can include regular financial reporting, access to information, limits on major business changes, and a clear covenant on how the buyer will operate the target during the earn-out period. The right balance depends on the deal, the sector, and how involved the seller will remain.

Final thoughts

Earn-outs can bridge a valuation gap and keep a UK M&A deal alive when price is the sticking point. Their true value, however, is not in the headline number—it is in whether the terms are clear, measurable, and fair after completion.

For owners planning an exit, the best time to shape the earn-out is early, before heads of terms lock in the wrong structure.

Want to structure a deal that actually pays out? Get in touch with Consult EFC today for expert corporate finance support to ensure the deal you sign is the outcome you actually collect.

Not sure where your business stands right now?

Book a free 30-minute call with Kish. Bring your numbers, your questions, or just your situation. You will leave with a clearer picture than you arrived with.

Book a Free Strategy Call

Over 12 years across Big Four audit, Investment Banking, and corporate advisory. Kish works with SaaS founders, tech companies, and ambitious UK SMEs from £1M to £50M in revenue on fundraising, valuations, exit planning, and financial strategy. ICAEW regulated. Big Four trained. Based in London.