A term sheet is defined as a preliminary, mostly non-binding document that summarises the key economic and control terms of a proposed investment before any binding legal contracts are drafted. Every UK founder seeking external funding will encounter one, yet few read it with the attention it deserves. The document covers everything from valuation and liquidation preferences to board composition and voting rights. Two clauses, confidentiality and exclusivity, are binding immediately upon signing and can restrict your options for weeks. Understanding a term sheet before you sign is not optional. It is the foundation of your company’s future governance and financial structure.

What is a term sheet and what does it include?

A term sheet is a blueprint for definitive agreements such as stock purchase agreements and shareholder documents. It does not close the deal. It sets the terms on which both parties agree to proceed towards closing. Most term sheets run between 5 to 15 pages and are divided into two broad categories: economic terms and control terms. That structure exists to make negotiation cleaner and to reduce the risk of misunderstanding later.

Economic terms

Economic terms govern how money flows in and out of the company. The core components are:

- Valuation. The pre-money valuation determines your equity stake after investment. A higher valuation is not always better if it comes with aggressive investor protections elsewhere in the document.

- Liquidation preference. This clause determines who gets paid first, and how much, when the company is sold or wound up. Participating vs non-participating preferences can dramatically alter what founders receive at exit.

- Pro-rata rights. These give investors the right to participate in future funding rounds to maintain their ownership percentage.

- Anti-dilution provisions. These protect investors if the company raises money at a lower valuation in a future round.

Control terms

Control terms govern who makes decisions. They include board composition, voting rights, and veto powers over major decisions such as acquisitions, new share issuances, or changes to the company’s articles. Founders who overlook these clauses often find themselves unable to act without investor approval on decisions they assumed were theirs alone.

Pro Tip: Read every veto right listed in the control terms section. A single broadly worded veto can give an investor effective control over your company without holding a majority of shares.

The two clauses that are binding from the moment you sign are confidentiality and the no-shop provision. The no-shop clause prevents you from approaching other investors for a defined period, typically around 30 days. That window freezes your fundraising options and concentrates your negotiating position entirely on this one investor.

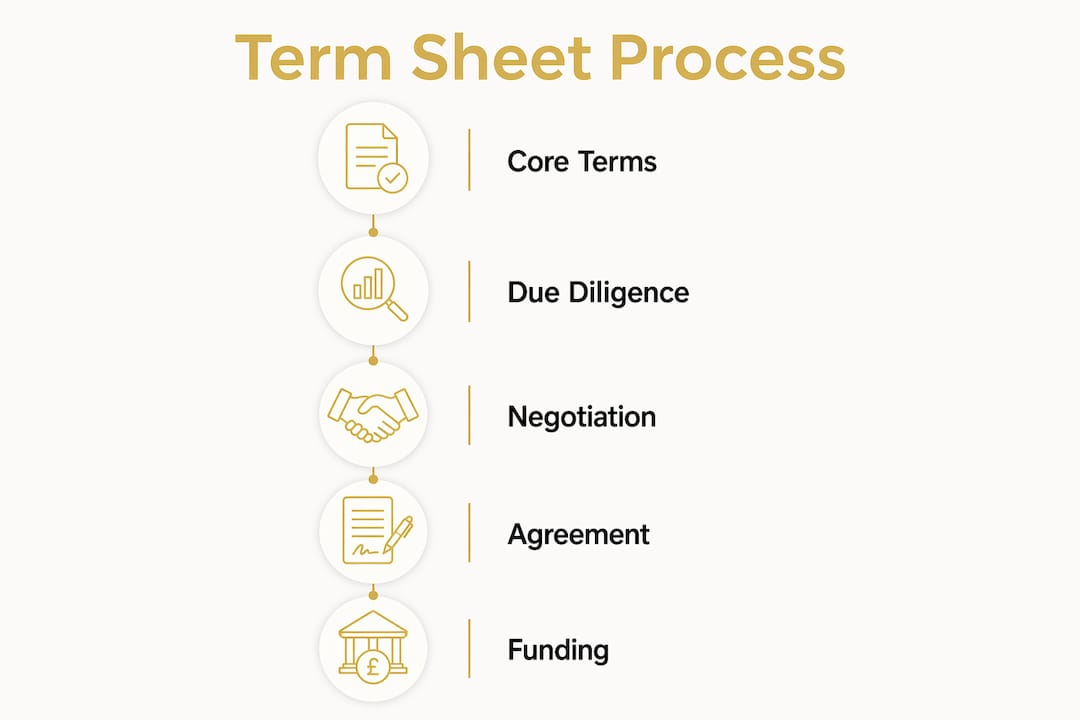

How does a term sheet fit into the investment process?

The investment process follows a clear sequence. You negotiate the term sheet, sign it, then move into drafting definitive legal documents. The term sheet sits at the hinge between informal discussion and formal legal commitment.

- Initial discussions. You and the investor agree on broad deal parameters through conversations and pitch meetings.

- Term sheet issued. The investor sends a term sheet reflecting their proposed terms. This is the start of formal negotiation, not the end.

- Negotiation and signing. Both parties negotiate the terms, then sign the document. Binding provisions take effect immediately.

- Exclusivity period. The no-shop clause activates. You cannot approach other investors during this window, which typically lasts around 30 days.

- Definitive agreements drafted. Lawyers use the signed term sheet as the baseline for all binding legal contracts. The terms agreed here govern every document that follows.

- Closing. Funds are transferred and the deal is complete.

The term sheet reduces upfront legal costs by forcing both parties to agree on core terms before expensive drafting begins. That is its practical function. A signed term sheet also shifts the psychological dynamic of the negotiation. Both parties treat it as a commitment, even though most of it is technically non-binding. Renegotiating after signing is possible but carries real risk of damaging trust or collapsing the deal entirely.

The due diligence checklist for UK founders is a useful companion at this stage, helping you prepare your financial and legal documentation before the exclusivity clock starts ticking.

What are the common misconceptions founders should know?

The most damaging misconception is that receiving a term sheet means the deal is nearly closed. Receiving a term sheet signals the start of the most critical negotiation phase, not the end of it. Founders who treat it as a formality often sign terms they later regret.

The second major mistake is fixating on valuation at the expense of everything else. Founders often direct the vast majority of their negotiation energy towards the headline valuation figure. Control rights and liquidation preferences deserve equal attention. Here is why that matters:

- Liquidation preferences determine exit proceeds. A participating liquidation preference means the investor takes their preferred return first, then participates again in the remaining proceeds alongside ordinary shareholders. Even a high valuation can be undercut by an aggressive participating preference at exit.

- Board composition shapes your future. If investors hold a board majority from Series A, they can remove the CEO, block acquisitions, or override strategic decisions. This is not hypothetical. It happens regularly in UK startup funding rounds.

- Veto rights accumulate. Each funding round can add new protective provisions. Founders who accept broad vetoes early find them compounding across later rounds.

“Valuation is the number everyone talks about in the room. Liquidation preferences and board control are the numbers that matter when the room is empty and the company is being sold.”

Pro Tip: Before entering term sheet negotiation, review your cap table carefully. Knowing your current ownership structure helps you model the real impact of proposed economic terms before you agree to anything.

Negotiating professionally and transparently at this stage sets the tone for the entire investor-founder relationship. Investors expect founders to push back on unfavourable terms. A founder who accepts everything without question raises concerns about their commercial judgement, not confidence in their agreeableness.

What practical steps should founders take with a term sheet?

Managing a term sheet well requires discipline and preparation. These steps reduce the risk of signing something that constrains your company for years.

- Read every clause before responding. Do not skim. Economic and control terms interact with each other. A favourable valuation paired with a 2x participating preference and a broad veto list can leave founders worse off than a lower valuation with cleaner terms.

- Identify which provisions are binding. Confidentiality and no-shop clauses bind you immediately. Everything else is a negotiating position until the definitive agreements are signed.

- Do not rush the signature. Founders who rush to sign trigger binding provisions and lock in terms that govern their company for years. Take the time to review properly, even if the investor signals urgency.

- Model the economics at exit. Run scenarios using the proposed liquidation preference structure. A business valuation exercise at this stage helps you understand what different exit prices actually mean for founder proceeds under the proposed terms.

- Negotiate governance alongside economics. Push for a balanced board structure. Seek to limit veto rights to genuinely material decisions. Governance terms are easier to negotiate now than after closing.

- Prepare for the exclusivity period. Once you sign, you cannot approach other investors for around 30 days. Before signing, exclusivity clauses effectively freeze your fundraising options. Make sure you are comfortable with this investor before the clock starts.

- Seek expert advice. A fractional CFO or specialist lawyer who understands UK venture capital norms can identify non-standard terms quickly and advise on what is worth pushing back on.

Common value investing mistakes apply here too. Founders, like investors, often overweight headline numbers and underweight structural terms that determine actual outcomes.

Key takeaways

A term sheet is the single most consequential document in an early funding round, and the terms agreed within it form the baseline for every binding legal contract that follows.

| Point | Details |

|---|---|

| Mostly non-binding, but not entirely | Confidentiality and no-shop clauses bind immediately upon signing, typically for around 30 days. |

| Economic terms go beyond valuation | Liquidation preferences and anti-dilution provisions often determine founder proceeds at exit more than the headline valuation. |

| Control terms shape governance | Board composition and veto rights determine who makes key decisions long after the deal closes. |

| Signing starts the clock | The exclusivity period freezes fundraising options, so founders must be confident before signing. |

| Negotiation is expected | Investors expect founders to push back on unfavourable terms; accepting everything signals poor commercial judgement. |

Term sheets and the long game: a perspective from Kishen Patel

Every week I speak with founders who treat the term sheet as a milestone to get past rather than a document to get right. That mindset is the single most expensive mistake I see in early-stage funding rounds.

The term sheet is a social contract. Yes, most of it is non-binding in a strict legal sense. But in practice, renegotiating after signing risks the entire deal and damages the relationship before it has properly started. The terms you agree here follow your company through every subsequent round, every board meeting, and every exit conversation.

What I tell founders is this: spend as much time on the governance section as you do on the valuation. A £10m pre-money valuation with a 2x participating preference and investor board control is a worse deal than an £8m valuation with clean terms and a balanced board. The maths are not complicated once you model the exit scenarios properly.

The founders who negotiate well are not the ones who push hardest on price. They are the ones who understand what they are agreeing to and ask precise questions about every clause. That is the kind of financial literacy that protects your company for years. It is also, frankly, what investors want to see. A founder who understands their term sheet is a founder who will understand their business.

— Kishen Patel

How Consult EFC supports founders through funding negotiations

Raising a funding round is one of the most consequential periods in a founder’s career. Getting the financial strategy right before and during that process makes a material difference to the outcome.

Consult EFC provides fractional CFO services for startups that cover exactly this territory. From building investor-ready financial models to reviewing term sheet economics and advising on governance structures, the firm brings ICAEW-level rigour to founders who need expert guidance without the cost of a full-time CFO. If you are approaching a funding round and want to understand what you are signing before you sign it, Consult EFC offers the kind of experienced, independent perspective that protects founders and strengthens their negotiating position. Learn more about fractional CFO services and how they apply to your funding stage.

FAQ

What is a term sheet in business?

A term sheet is a preliminary document that outlines the proposed economic and control terms of an investment before binding legal agreements are drafted. It is mostly non-binding, except for confidentiality and exclusivity clauses which take effect immediately upon signing.

Are term sheets legally binding in the UK?

Most provisions in a UK term sheet are non-binding and serve as a negotiating framework. However, no-shop and confidentiality clauses are typically binding from the moment of signing and can restrict founder activity for around 30 days.

What is the difference between a term sheet and a shareholders’ agreement?

A term sheet outlines the proposed terms of an investment in summary form. A shareholders’ agreement is the full, legally binding contract drafted after the term sheet is agreed and signed by all parties.

Why do liquidation preferences matter more than valuation?

Liquidation preferences determine how exit proceeds are distributed before ordinary shareholders receive anything. An aggressive participating preference can reduce founder returns significantly, even when the headline valuation appears favourable.

How long does a term sheet exclusivity period last?

Exclusivity periods in term sheets typically last around 30 days. During this window, founders cannot approach other investors, which concentrates negotiating leverage with the investor who issued the term sheet.

Recommended

- VC Term Sheet Red Flags UK Founders Must Spot (2026) | Consult EFC

- Working Capital in Term Sheets and SPAs: Protect Your Exit Price 2025

- LTV:CAC Benchmarks for 2026: What SaaS Founders Get Wrong

- Prepare for a Series A: Founder’s Playbook | Consult EFC

Not sure where your business stands right now?

Book a free 30-minute call with Kish. Bring your numbers, your questions, or just your situation. You will leave with a clearer picture than you arrived with.

Book a Free Strategy Call

Over 12 years across Big Four audit, Investment Banking, and corporate advisory. Kish works with SaaS founders, tech companies, and ambitious UK SMEs from £1M to £50M in revenue on fundraising, valuations, exit planning, and financial strategy. ICAEW regulated. Big Four trained. Based in London.